My last post (published over a BA ago) referenced the Keynesian Consumption Function in its approach. The eponym of this laughably oversimplifying economic assumption is largely unknown to those outside of the dismal science. Yet, I believe there exists a compelling argument to consider John Maynard Keynes the next time you’re asked for your dream dinner guest.

Born to a middle class family in Cambridge, Keynes won a scholarship to study at Eton. From there, he returned to Cambridge to study Mathematics at King’s. During this time, he was president of the University Liberal Club, president of the Union, and a member of the University Pitt Club. He was also an active member of the Cambridge Apostles during what many consider to be its heyday. This most secret of Cambridge societies was founded by George Tomlinson (an Olavian-Johnian1 like myself) in 1820 for the most learned of Cantabrigians to engage in highbrow chat. Around a century later, the mother of an Apostle called it a “hotbed of vice” upon discovering her son’s letters. Nevertheless, Keynes’s Cambridge was undeniably a hotbed of intellectual activity. He graduated with a first and continued to be involved with the university for some time, attending economics lectures as a graduate having been urged to do so by the famously sexist economist, Alfred Marshall.

Over the following few decades, Keynes essentially fathered the modern field of macroeconomics. He argued that the government had a role to play in attenuating the business cycle by implementing counter-cyclical policy. Why? Well basically because people don’t like to see the key number on their pay slip go down. Don’t see how these two things are linked? Unfortunately, explaining why in simple terms is beyond my writing and economics abilities. You will have to ask a “macro specialist” – I know one or two who I can get you in touch with if you’re really interested.

Keynes’s magnum opus, The General Theory of Employment, Interest and Money essentially made him a post-Depression celebrity. The rejection of the neoliberal laissez-faire paradigm caught on. In April 1942, Keynes joined the Bank of England and in June he was rewarded for his service with a hereditary peerage in the King’s Birthday Honours. He took his seat in the Lords on the Liberal Party benches (don’t let this stop you from reading on).

Caricature of Keynes by David Low, 1934

Following the war, Keynes and his idea in The General Theory were crucial in establishing the post-war global order. Keynes was heavily involved, as leader of the British delegation and chairman of the World Bank commission, in the mid-1944 negotiations that established the Bretton Woods system. He also proposed the creation of a common world unit of currency, the bancor and new global institutions. Although these did not materialise immediately, they were essentially manifested in the creation of the IMF and its Special Drawing Rights (SDR) function. Keynes rubbed shoulders (or more likely elbows at his towering height of 6ft 7) with the likes of FDR and negotiated fiercely with Harry Dexter White. He was able to obtain a preferential position for Britain but ultimately failed to implement his ideas globally. Despite this, Keynes was crucial in constructing the global world in which we live today.

P. G. Wodehouse at Dulwich College

This is all very interesting; all very impressive. But it’s Keynes’s views on leisure2 that have really stuck out to me lately. For my own leisure, I picked up some P. G. Wodehouse this Christmas. Envious of Bertie Wooster’s position as a societal drone I was reminded of Keynes’s 1928 essay Economic Possibilities for our Grandchildren. He posits that one day “the economic problem may be solved” and that “for the first time since his creation man will be faced with his real, his permanent problem-how to use his freedom from pressing economic cares, how to occupy the leisure, which science and compound interest will have won for him”. Keynes was no stranger to leisure; he had a passion for theatre, ballet, art, literature and philosophy which he shared with the likes of E. M. Forster and Virginia Woolf as a part of the Bloomsbury Set.

46 Gordon Square, Bloomsbury, London where Keynes lived from 1916

I wonder what Keynes would have thought about the recent developments in AI which is most certainly the type of science he anticipated in his essay. For the purpose of this post, let us assume away the bleak complications threatened by AI. I, for one, am hopeful. And I suspect Keynes would share my sentiment; he was considered by many an unbending optimist. He would have been particularly grateful for more time to indulge in the arts with his Bloomsbury chums. Taking a sporting view, I envision the demise of T20 cricket and the return of the superior format to the top of the agenda as hundreds of millions of fans are released from the shackles of work. Although could this go too far? Would these fans start reading through their copies of Wisden at a loss for what to do?

Tomlinson was at St Saviour’s school before its amalgamation with St Olave’s. ↩︎

Leisure is an economist’s word for anything that isn’t paid work. ↩︎

As a part of the Coronavirus Aid, Relief and Economic Security (CARES) Act, the US Federal government made one time payments directly to households. A relatively high income threshold meant that most Americans were eligible for a payment with adults receiving a payment of $1200 and children receiving $500. The intended effect of these checks was to increase aggregate consumption in the US economy, easing economic decline as a result of the pandemic. We will examine the effectiveness of stimulus checks through the lens of a Keynesian consumption function and Friendman’s permanent income hypothesis (PIH). We will use evidence from households’ spending reports from a Fintech non-profit, a large scale survey of US households and aggregate evidence following the 2001 and 2008 tax rebates.

The Keynesian Consumption Function

Traditional macroeconomic theory would explain how stimulus checks would stimulate the economy through the Keynesian consumption function which takes the following form: C = a + b(Yd) where C is total aggregate consumption, Yd is real disposable income, a is autonomous consumption and b is the marginal propensity to consume (MPC). Stimulus payments, such as those included in the CARES Act, are intended to increase Yd, thus increasing households’ consumption. This will cause an increase in aggregate demand, lessening economic contraction during a recession. From the consumption function it can be seen that the effectiveness of the stimulus checks depends on the size of the MPC, with a larger MPC resulting in a larger increase in consumption (and larger multiplier effect) whilst a smaller MPC results in a smaller increase in consumption (and smaller multiplier effect).

Baker et al. (2020) use high-frequency transaction data from a Fintech non-profit, called SaverLife, to analyse the size of the MPC and how it is affected by income and liquidity. It should be considered that SaverLife users have relatively low income, with average disposable income of $36,000 per annum and median checking account balance of $98. The typical individual in the sample used by the researchers exhibited a rise in mean daily spending from $90 to $250 for the weekdays after receipt of the stimulus, with the increase in spending mostly driven by food and non-durables. The researchers also found that the MPC of SaverLife users varied greatly with level of income, with users having a monthly income above $2000 estimated to have an MPC of 0.325 whilst users with an income below $2000 per month estimated to have an MPC of 0.571. MPC also varied greatly with checking account balance, with users in the 4th quartile of checking account balance having an estimated MPC of 0.256 whilst those in the 1st quartile have an MPC of 0.468. These results may be useful in guiding targeted stimulus measures in the future in order to make stimulus checks more effective.

Coibion et al. (2020) consider a broader sample, using a large-scale survey of US consumers to study how stimulus checks affected consumption. When asked to break down how US households spent (or planned to spend) their checks, on average around 30% was saved, 30% was used to pay existing debts and the remaining 40% was spent on consumption. In short Coibon found that the average MPC out of stimulus payments was little over 0.4 with almost 40% of respondents having a MPC of 0.

Therefore, we can see that both the data from SaverLife and the large scale survey suggest that the MPC out of stimulus payments was low, reducing the effectiveness of the policy. We can potentially explain this by using the permanent income hypothesis.

The Permanent Income Hypothesis

Unlike the Keynesian consumption function, which believes that current levels of consumption depend only on current levels of income, Friedman’s permanent income hypothesis believes that consumers consider expected future levels of income when deciding what proportion of their marginal income to spend on consumption. Under the PIH model, a temporary increase in income will only result in a small increase in present consumption as future income expectations are unimpacted. Consumers will save the majority of the temporary increase in income to smooth consumption in the future. The model requires a rise in permanent income (long-term expected income) for consumption to rise. This may arise from an increase in wage levels or the introduction of a universal basic income for example. Therefore, the PIH model predicts that stimulus checks, a form of temporary income, will have little effect on current levels of consumption.

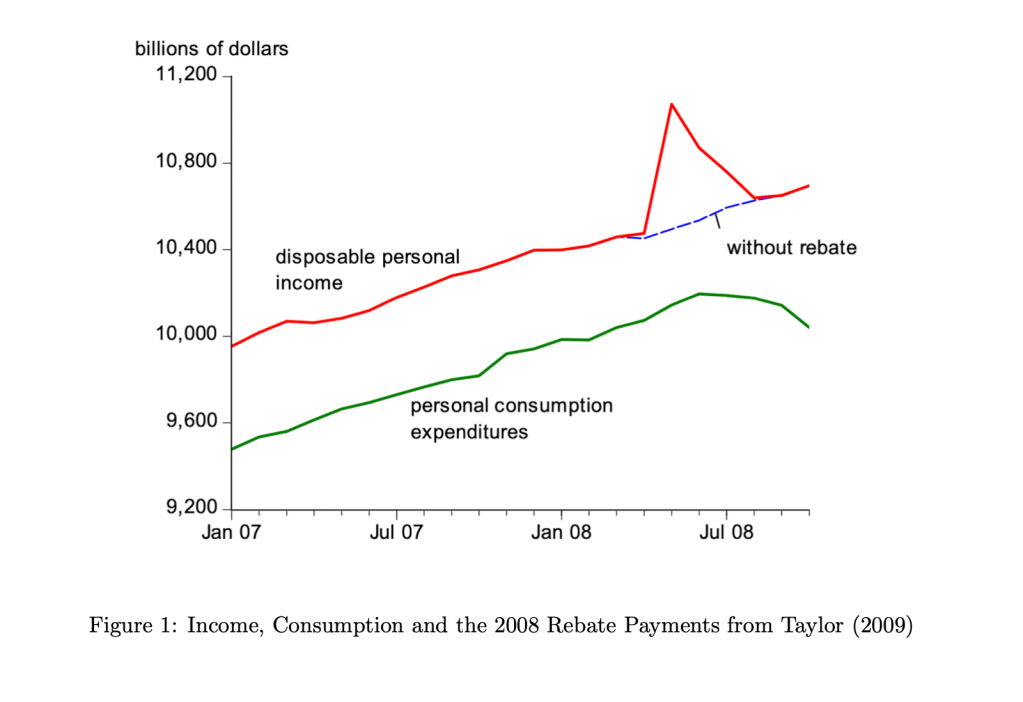

We can look at aggregate consumption data following tax rebates in 2001 and 2008 to confirm these predictions. In May of 2008, as part of the Economic Stimulus Act of 2008, tax rebates were made to households. Figure 1 shows that the temporary rebate had little to no effect on aggregate consumption. A more formal regression technique by Taylor (2009), which corrected for changes in oil prices, also found the rebates to be insignificant. When Taylor conducted a regression using disposable income minus the rebate (permanent income) he found the increase in consumption to be statistically significant. These findings are consistent with the PIH model.

As part of the Economic Growth and Tax Relief Reconciliation Act of 2001, most American taxpayers received checks of up to $300 per individual. Shapiro and Slemrod (2003) used surveys to look for evidence of lagged responses. Of those who initially said they would mostly save their rebate, 93.4% said that they would try to keep up a higher saving (or lower debt) for at least a year, when asked 6 months later.1 This is consistent with the PIH model. Shapiro and Slemrod (2009) carried out a similar survey in 2008, in which only 18% of those who said they were saving the rebate said they would spend it later. Therefore, in both 2001 and 2008 consumers did not expect to spend their rebates. This is consistent with the predictions of the PIH model as consumers would only spend if increases in income were permanent.

Conclusion

It is clear from the evidence used that stimulus checks are ineffective at stimulating aggregate consumption, as past uses of stimulus checks have rendered low MPCs which can be explained through the PIH. This low MPC means that the aggregate effect of the policy is low (due to a small multiplier effect) and also means that the policy provides little “bang for the buck” when fiscal resources are scarce. In the future it may be possible to target such stimulus at those with lower liquidity or income who exhibit higher MPCs. Despite this MPCs will still remain relatively low due to the income being temporary. Instead, policies that increase wages, a form of permanent income, should be considered.

Economic theory tells us that money has three primary functions, to act as a medium of exchange, a store of value and a unit of account. The US Dollar not only excels in these three functions, but it also dominates against every other currency globally. In 2019, the greenback was involved in 88% of international transactions and 40% of the world’s debt is issued in dollars. Amazingly, in 2018, the banks of Germany, France and Britain held more liabilities in dollars than their own currencies. The dollar excels as a medium of exchange, both in the goods and capital markets. Around 60% of total central bank foreign exchange reserves are allocated in dollars. Even during the Great Recession, the dollar strengthened by 22%, despite the crisis originating from the US. The dollar has proved to be an excellent store of value throughout the boom-bust cycle. The dollar also thrives as an invoicing currency, with over 50% of goods imported into the EU being invoiced in dollars despite the Euro being the world’s second most dominant currency. Furthermore, numerous commodities such as oil, gold and coffee are priced in dollars, making it an almost universally understood unit of account. The dollar is irrefutably the king of currencies, but will the effects of coronavirus reaffirm this or bring the dollar’s reign to an end?

A cartoon by The Economist

Economist Charles P. Kindleberger argued that a dominant currency would actively stabilise the global economy by promoting trade and supporting capital markets in his “hegemonic stability theory”. The impacts of the dollar hegemony prove him right. Take two foreign companies who desire to trade. Two things may stand in their way. A volatile exchange rate between their two domestic currencies, exposing them to foreign exchange risk and the difficulty of trading two uncommon currencies. If both firms use the US dollar, these barriers are eliminated, thereby promoting trade. For this reason, more countries and firms are incentivised to operate in dollars, stimulating global trade and facilitating growth across the world.

Unsurprisingly the US itself can derive some benefits from the widespread use of its currency – it’s so-called “exorbitant privilege”. The dollars reserve status means that central banks and foreign governments flock to buy US Treasuries, driving down the cost of borrowing for the government. Estimates by McKinsey suggest that the US governments borrowing costs have been reduced by 0.5 – 0.6% in recent years due to the dollar’s reserve status. The dollars use in international transactions also provide the currency with greater liquidity, reducing the cost of private borrowing in USD, benefiting capital accumulation, and thereby economic growth.

However, dollar primacy is not without its drawbacks. Continued demand for the US dollar for FX reserves and international trade inflates the currency’s exchange rate from 5-10 percent. This results in less price competitive US exports and more price-competitive imports, contributing to the US’ persistent current account deficit. Furthermore, dollar primacy can lead to the transmission of monetary policy enacted by the Fed around the world. Although this may sound appealing at first, Ben Bernanke argues that we need to ensure the Fed doesn’t become the “world’s central bank”. Take contractionary policy by the Fed. An increase in the interest rate will cause a currency appreciation due to hot money flows. This results in larger debt burdens for emerging market borrowers, with 33% of corporate bonds in EMEs denominated in dollars. This can depress capital accumulation and unintentionally slow global economic growth.

In past global crises, America has successfully coordinated international responses, proving its worthiness as the world’s economic and geopolitical superpower. During the COVID-19 crisis, it has done much the opposite. After botching its domestic response, the Trump administration has failed to support developing economies, erratically cut funding for the World Health Organisation and engaged in a dangerous blame game with China. This glaring ineptitude of American leadership has left a void in global initiative – one many nations will attempt to fill.

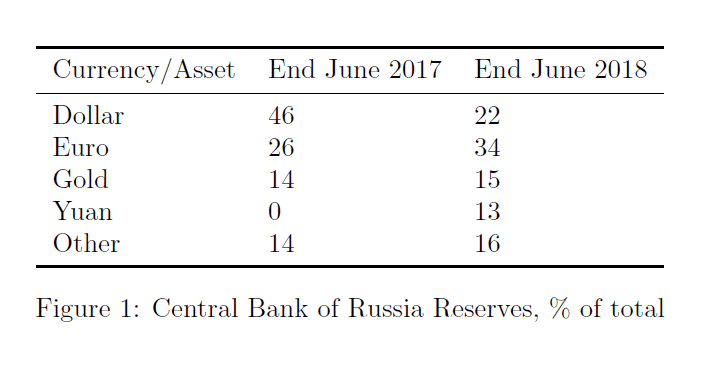

China is hastily trying to reshape its image as the world’s saviour, not the deliverer of its demise. It has distributed vital medical provisions and teams of medical experts to disproportionately impacted regions. Alibaba and Huawei, who have often been cited as henchmen of the Chinese Communist Party (CCP), have donated supplies to nations in Africa, South East Asia and even Europe in a bid to win over sceptics. With this reshaping of its image, China will promote the renminbi as an alternative to the dollar. Early signs are showing this at work. In late February, as the virus emerged in Europe, foreign investors poured $10.7 billion into China’s yuan-denominated bond market – a potential new safe-haven asset. Moreover, the People’s Bank of China (PBoC) has shown restraint when expanding the money supply. The PBoC is reluctant to monetise the Chinese budget deficit or expand their balance sheet, making the yuan an even more attractive reserve currency option. Russia has already begun to de-dollarise parts of its financial system in favour of the yuan. The Russian Central Bank’s holdings of the dollar fell from over 40% in 2017 to 22% in mid-2018, with the central bank taking up a greater position (nearly 15%) in yuan. Russia has also explored settling more of its bilateral trade in its own currency – the rouble, and has even considered issuing its sovereign debt in yuan. Russia has shown that the yuan is a worthy contender for the dollar as a reserve currency – one that other governments and monetary authorities should start to strongly consider.

In early May, the PBoC began trials of its new cryptocurrency – the e-RMB. It is set to be the first digital currency operated by a major economy and represents a huge step away from the dollar hegemony. Chinese officials are unashamed to reveal the true intentions of this technology. The state-run China Daily reported that “A sovereign digital currency provides a functional alternative to the dollar settlement system and blunts the impact of any sanctions or threats of exclusion”. Its adoption may be appealing for other nations (or firms) trying to distance itself from the political volatility in Washington DC.

However, the ugly side of the autocratic state should not be ignored. Many developing nations are already weak from Chinese “debt-trap diplomacy”. The pandemic may exacerbate this with China providing debt relief at the cost of sovereignty – already seen prior to the pandemic in Sri Lanka and Djibouti. Furthermore, the power continues to undermine the independence of Hong Kong; a move that may be financially motivated, given that the financial centre lives and breathes off the dollar. As Chinese control tightens in the Special Administrative Region, we may see an increase in the use of the yuan in its cross-border financial dealings. Furthermore, China continues to expand its operation in the South China Sea and continues to commit human rights violations against its Uyghur Muslim minority. For these reasons, most western democracies will not have the confidence in China to adopt the yuan to the extent Russia has.

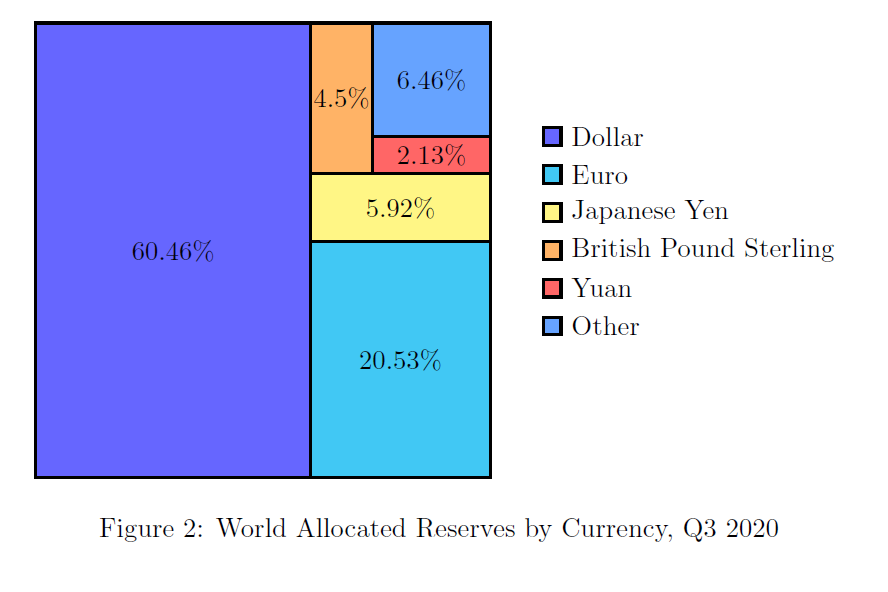

It is not only the US’s adversaries that are posing a threat to dollar primacy. As can be seen from Figure 2, the euro is already the dollar’s strongest competitor, making up 20% of central bank holdings against the dollar’s 62%. As US politics has become increasingly dysfunctional, the European Union (EU) has shown unprecedented solidarity by agreeing upon a budget and recovery fund worth €1.82 trillion. For the first time, the bloc will raise €750 billion with collective EU bonds – a reserve instrument that, in time, may be able to match the liquidity and security of US treasuries. Stephen S. Roach of Yale University believes that this fiscal breakthrough will “drive an important wedge between the overvalued US dollar and the undervalued Euro”. Furthermore, the EU has largely succeeded in curtailing the spread of COVID-19 and is planning a large scale “green recovery” as part of its budget. This is in stark contrast to the US, which approaches a fiscal cliff edge as the provisions from the CARES act expire and congress fail to pass further measures. For these reasons, investors are becoming increasingly confident about the prospects for the Eurozone economy. Consequently, the euro has strengthened 9% against the dollar since the recovery fund was first proposed.

The global pandemic also threatens one of the factors that has made the dollar so great – globalisation. Measures taken by governments to curtail the spread of COVID-19 has brought upon the fastest decline in cross border economic activity in history. We have seen unprecedented falls in merchandise trade, foreign direct investment (FDI) and air travel. The outlook for globalisation in the post-COVID world is also bleak. Many US firms will likely decide to re-nationalise supply chains, prioritising resilience to external shocks over efficiency. Firms in key industries such as health and national security may be egged on to do so by the Trump administration, through subsidies for repatriating factories (as seen in Japan). This will disrupt the flow of dollars to manufacturing and export-orientated economies, thereby disrupting the flow of dollars around the world. This sudden shift in the availability of the dollar epitomises what nations like China and Russia fear the most regarding dollar primacy. And thus, it follows that COVID-19 will accelerate the adoption of alternatives to the dollar, whatever form they may take.

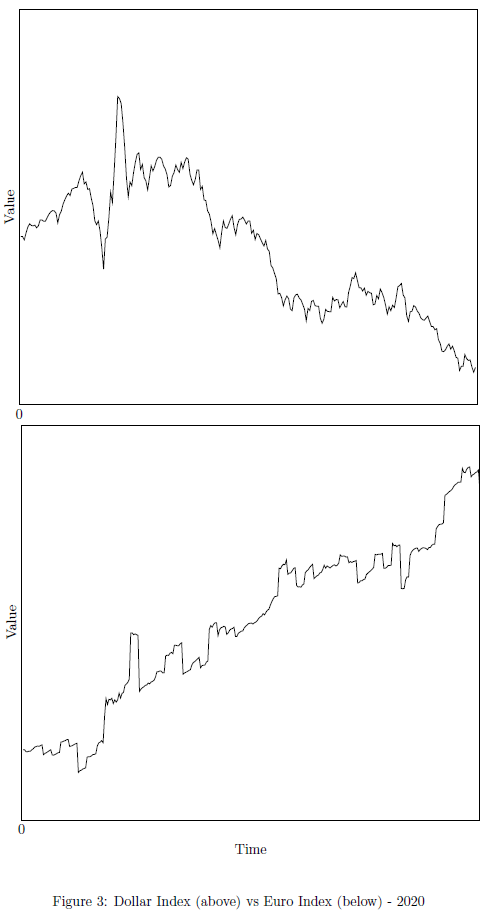

Although COVID-19 does pose a threat to the dollar, there is little chance the pandemic will trigger a total overhaul of the world monetary system. In fact, the pandemic has highlighted many of the dollar’s unique selling points. As the economic implications of the pandemic first became clear, demand for the dollar skyrocketed. This is despite massive deficit spending and the expansion of the Fed’s balance sheet that should have theoretically devalued the currency. The DXY index, which measures the dollar against a basket of other currencies, was up by as much as 6.5% from the beginning of the year to March. This shows the extreme, potentially unjustified, confidence in the greenback as a store of value. In conjunction with this, the Fed has acted swiftly and proactively – unlike its colleagues in Capitol Hill – to ensure the smooth running of the global financial system. It “coordinated central bank action to enhance the provision of US dollar liquidity”, arranging bilateral currency swaps and repurchasing facilities with fourteen foreign central banks. No foreign currency – least likely one managed by the CCP – will instil the level of confidence, liquidity and openness required to challenge the dollar. If Americans choose to elect a new president in November, we will most likely see a shift to a less insular form of foreign policy, thereby blunting the long-term effects of COVID-19 on dollar primacy.

The pandemic is exposing – and widening – the cracks in the US’ grip on the global monetary system. Following its March rally, the DXY has fallen by over 10% whilst, in the same time period, the EXY, which measures the euro against a basket of other currencies, is up over 10%. The inertia of the dollar’s dominance, that has prevailed since Bretton Woods, has certainly been disrupted. The unstoppable rise of the dollar in the twentieth century reflected the rise of the current global order and the pre-eminence of the USA, both of which have been brought into question by the pandemic. However, alternatives to the dollar are still in their early stages. It is important to keep in mind that a currency’s utility is largely defined by its existing presence. In this regard, the dollar is virtually unassailable. Therefore, we will not see a sudden ascent to power by a rival currency. Instead, we will see a slow erosion of the dollar’s position at the helm of international finance.